Heads or tails you lose: How finance executives can avoid the AI double trap

The AI adoption trap: executives are forced into one of two extreme options

In the late 2000s I worked in wholesale banking strategy for a global bank in Nigeria. For years, the local leadership team lamented how difficult it was to compete against large local banks with massive branch networks. For reference, we had just under 3% of the branch network of the largest local players.

Eventually, the global team signed off on significant investment into expanding branch network and the new branches launched to huge fanfare. Good news right! Yes, but only for a short while. By 2016, the bank had closed 30% of its branch network due to “underperformance.” So in a span of six years the bank went from “we need more branches” to “actually, no one uses our branches”. Apparently, we had spent years fighting the wrong battle.

A derelict bank branch

While we were building branches to become more competitive, the mobile banking revolution was underway and reshaping banking. Revolut started in 2015 as a travel card startup but is now a fintech giant said to be valued at close to $100 billion. In Nigeria, names like Flutterwave, Moniepoint and Paystack did not exist in 2015. Today, they are well funded, well-known fintechs setting the standards around merchant acquisition and instant transfers. At the end of 2025, the bank I worked for had about 10% of the number of branches it had at its peak in 2016.

Just as the internet era and mobile apps have shaped the past two decades in banking, it is now obvious that generative AI will be a larger disruptor in the next few years. I see history repeating itself as many senior executives are making the same mistakes we made with branches a decade ago. They are completely ignoring the GenAI threat, either because they think it will be another passing fad or it’s too complex for them to wrap their heads around.

Interestingly, there is another trap some finance executives have fallen into at the extreme end from the first. These are leaders that jumped on the AI bandwagon early. They took the lesson literally and mandated their organisations to use generative AI soon after OpenAI’s ChatGPT launched in late 2022. You would think their firms would be enjoying the strategic advantage of being early in transformational technology. Except that many have wasted millions of dollars in investments with nothing to show for it.

Christin Owings, UK chief executive of Boston Consulting Group, told The Sunday Times that British businesses may have spent millions on AI adoption without knowing how to use it. A BCG study found that 74% of companies investing in AI have yet to show any tangible value from it. Christin’s observation was that leaders see excitement in pockets of the organisation and lots of individual use cases, but find it hard to translate any of that into increased profitability or productivity.

One investment banking managing director recently told me the frustration is that the associates aren’t using the tools the firm paid for as much as expected. Our conversation eventually led to what the problem was: the staff are only allowed to use Microsoft Copilot enterprise version. Copilot has its strengths but being locked into one tool is not going to excite associates who have access to the latest versions of Claude, Gamma, Openclaw and Google Gemini at home.

So banking leaders are caught between the proverbial rock and a hard place. Move too slowly and you risk being left behind and disrupted by new players. Move too fast and you end up in the same place, with the added challenge of having lost money on tools that nobody in the organisation actually wants to use.

AI adoption is currently very slow, the main challenge is integrating AI usage into the culture of the organisation — Partner, European Private Equity Firm

There is a middle path which very few executives are pursuing. The few who are doing so realise AI adoption is as much a cultural problem as it is a procurement problem. It’s not good enough to buy the latest, snazziest AI tools if no one is using them. The 26% from the BCG study who are seeing tangible results from AI adoption are those whose leaders have taken time to understand the technology before taking a decision on which parts of their workflows to enhance with AI and which tools support this. Let’s take a look at a three prong approach which separates the best from the rest.

Staying Competitive with Generative AI

1) Selective automation

Agentic banking promises AI tools that can completely run workflows from beginning to end without human involvement. Most of what we see are promises and theoretical applications with little in terms of demonstrated value from end-to-end process automation.

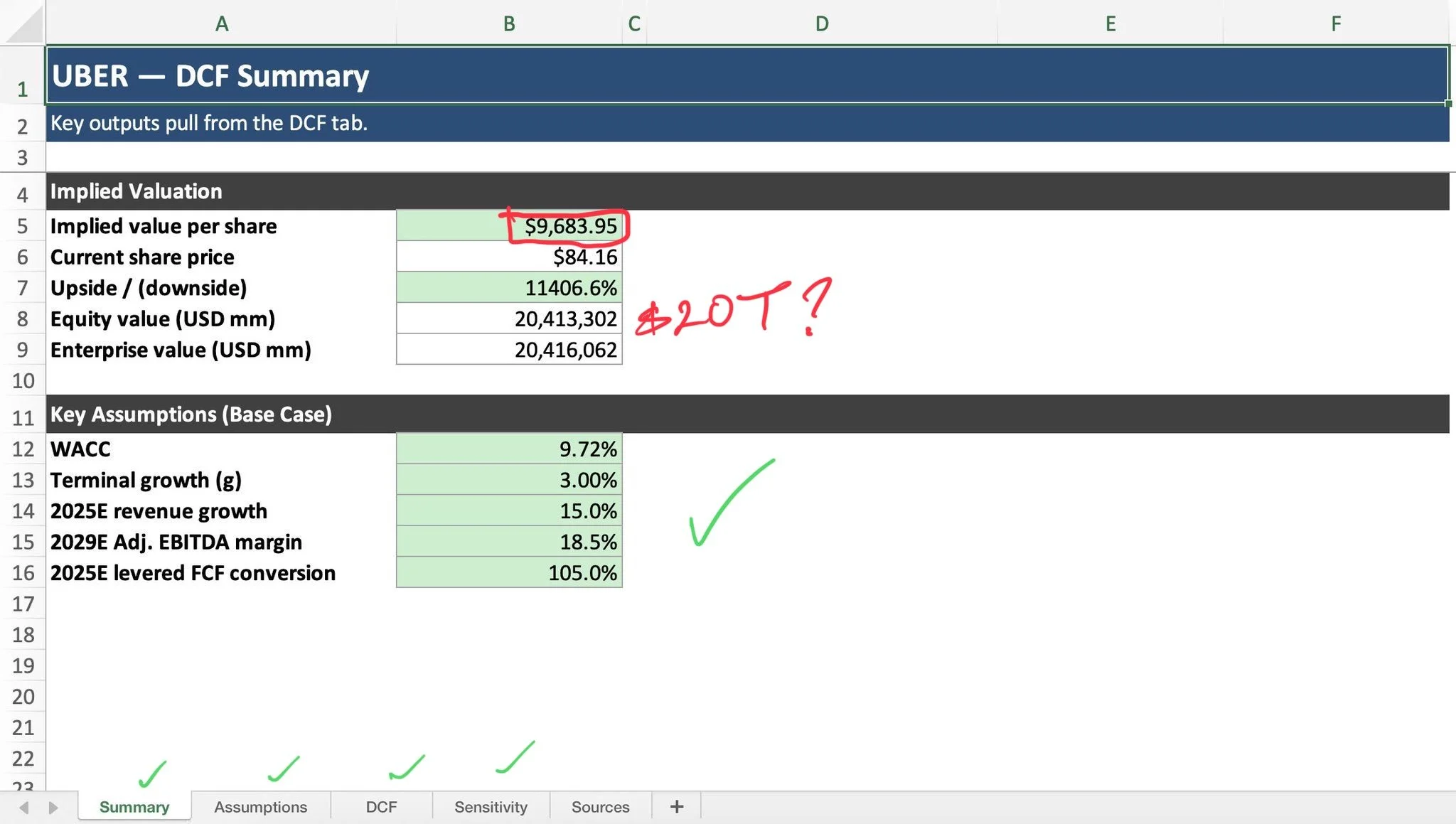

Let’s take investment banking, the large AI labs like OpenAI, Anthropic and Microsoft as well as specialist investment banking startups such as Rogo have invested significant sums in enabling their platforms to generate models from simple prompts. So far, the results have fallen short of the hype. For instance, when OpenAI demoed its GPT-5.2 Thinking model building a 5-year DCF for Uber in December 2025, the output returned an enterprise value of around $20 trillion against Uber’s actual market cap of roughly $177 billion, an implied upside of over 11,000%. This is a basic error any first year analyst would catch in seconds.

Faulty DCF demo’ed by OpenAI in December 2025

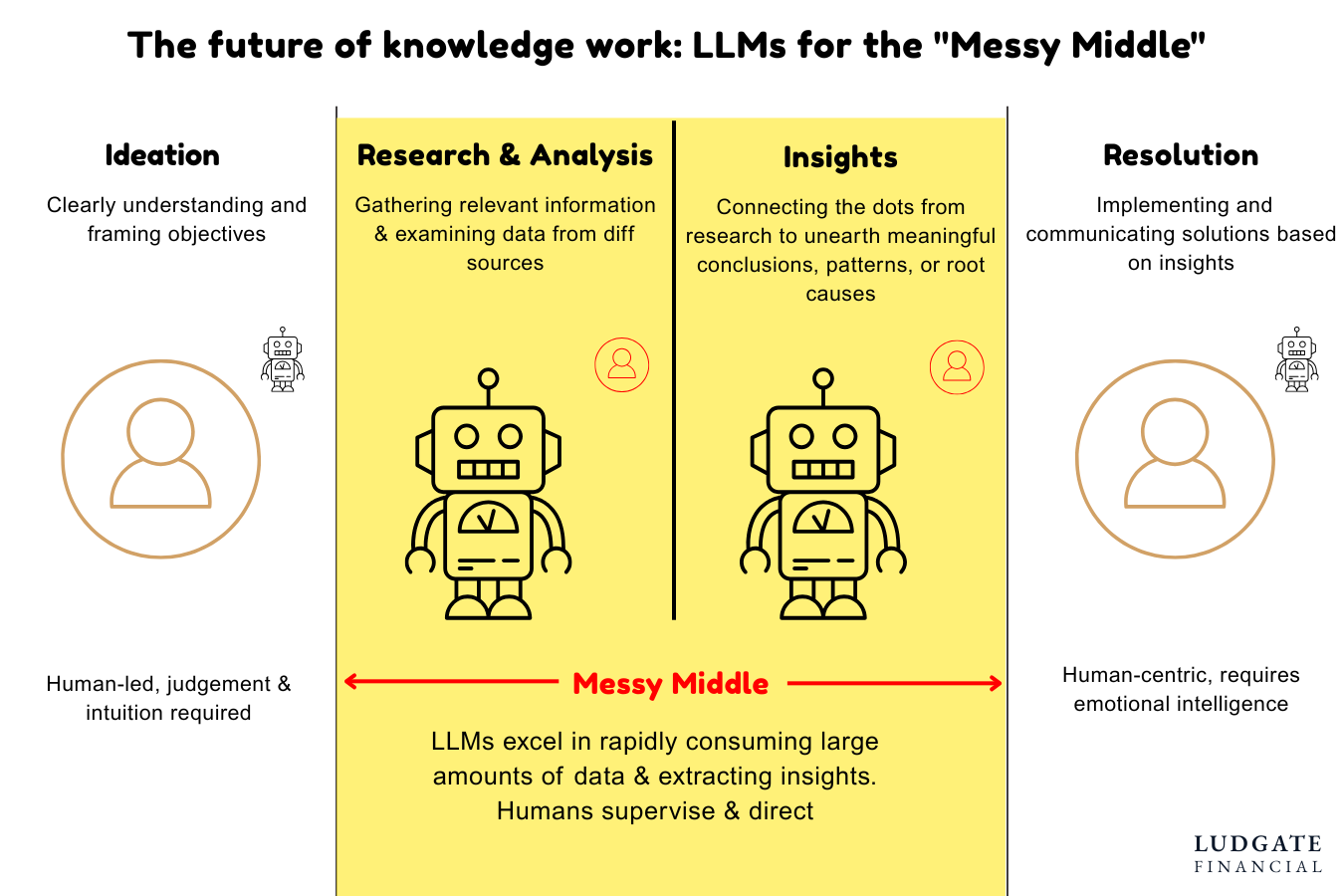

To get automation right, the first step is to have a good understanding of relative strengths and weaknesses of generative AI and decide which parts of discrete workflows are best to automate and which to leave as human led.

Messy middle: typical workflows need a combination of human judgement supported by AI automation

In the investment banking example, let’s say it takes a team of 3 investment bankers 5 days to conduct valuation and debt capacity analysis on Uber using the traditional, full human modelling in Excel. Reducing the TAT by 80% would mean empowering the team with different tools that are best suited to the specific time-consuming tasks such as research, data synthesis and data summarisation and visualisation. Designing and implementing this requires executives who fully understand the workflows as well as the AI tools landscape.

2) Embed AI Usage in Firm’s Culture

Partners and MDs could be forgiven for thinking they have done their part by doing the hard work of picking the right tasks to automate and mapping the right tools to them. Unfortunately, stopping there is a recipe for disaster.

The next critical step is to ensure the tools are adopted across their teams and become part of the culture. If you think this sounds difficult, then you’re absolutely right. The leaders who succeed in achieving adoption are those who lead by using the tools themselves. The BCG article makes the same point, noting that the few successful teams are those led by executives who use AI tools for at least eight hours a week.

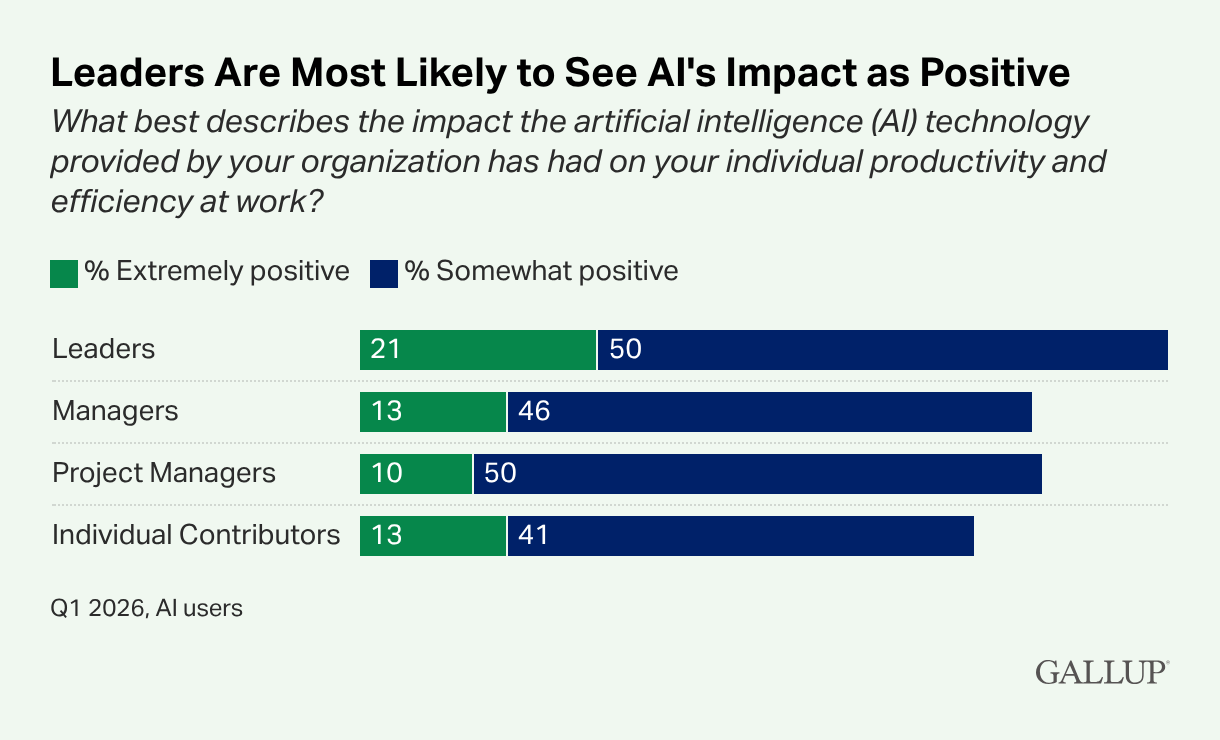

A recent poll from Gallup buttresses this point, it found that leaders are more likely to view AI's impact on productivity as positive than individual contributors. This means leaders who delegate the responsibility of championing AI transformation within their organisation stand the risk that the positive effects are not felt.

Gallup’s Feb. 4-19, 2026, survey of 23,717 U.S. employees

Too often, I’ve seen senior team leads take the easy way out by setting up a committee and delegating the task to a subordinate who is closer to the tools.

Using AI is a skill to be learnt, like Excel or public speaking — Director, Corporate Finance, Sovereign Wealth Fund

A director at a sovereign wealth fund who successfully got her team to use AI for a single task, research, told me what clicked for her was realising that using AI is a skill to be learnt, like Excel or public speaking. Taking the time to ensure she and her team were properly trained made a big difference in how smoothly the adoption went.

3) Focus on long term objectives

An investment banking VP (let’s call him Ali), whose MD had recently introduced an expensive AI tool told me the challenge he was dealing with was that he had to show a 50% reduction in delivery timelines within the first week. I could understand his frustration as achieving this goal was practically impossible.

The reality is that AI out of the box is a blank slate. LLMs get better and value compounds as they get configured with custom instructions and individual preferences. More importantly, the team needs to learn how the tools work and how to get the best out of them. This process takes time so demanding a 50% productivity gain in the first week is condemning the whole exercise to failure.

Ali and I worked through the problem together. We built the case for a realistic six month target with regular check-ins, giving the team the space to learn the tools properly while still keeping the MD close enough to the progress to stay confident in the investment. During the six month period, the team ended up hitting the target and went on to commission custom tools to automate other parts of the workflows.

AI is Here to Stay

The three steps are an iterative process, they are not one and done. More often than not, firms facing difficulties with adoption keep trying various tricks to get their teams using AI tools when in fact they should be going back to step 1. Conversely, a team that succeeds with their P&L or productivity objectives should go back to step 1 with the next step in their workflows.

Generative AI is here to stay and getting it right is existential for many firms. Being deliberate and methodical ensures you don’t fall into the trap of doing nothing due to paralysis or worse still failing despite investing heavily in the wrong tools. If you’re a banking leader working through this, feel free to book a confidential consultation session.